Portfolio Review – November 2020 – Issue 08

This is the latest One Four Nine Portfolio Management (OFNPM) portfolio review providing investors and advisers with an easy to digest overview of what’s happening in the markets globally, alongside comparisons of OFNPM’s portfolio performance each quarter and throughout the year.

Chief Investment Officer’s comments

In normal times a presidential election in the US that resulted in the incumbent losing would dominate headlines. Especially where the

incumbent did not concede the result and then proceeded to launch legal challenges, without any real basis or evidence, in multiple states on the premise that there was widespread electoral fraud. The ensuing uncertainty would dominate markets, increase volatility, reduce confidence and probably cause a sharp short-term drop in value.

Of course, the news that dominated the month was that 3 different vaccines, from Pfizer, Moderna and Astrazeneca, have shown that in

their third stages of clinical trials, all to be highly effective in the fight against the COVID-19 virus.

This news couldn’t come soon enough as the numbers of new virus cases continue to accelerate globally, especially in the US and Europe, resulting in the re-entering of full or partial lockdowns after a relaxed yet complacent summer in Europe.

The knock-on effect to Q4 GDP will not be mitigated by the news, but Q1 and Q2 GDP growth in 2021 should be better than would have been expected without it, as populations get vaccinated and economic life resumes something to resembling normality.

Economic outlook

Growth estimates for Q3 2020 GDP were mostly released in early November and they showed an expected rebound in all major economies as lockdown restrictions were eased. These increases in GDP however were smaller than the falls seen in the first half of the year.

Almost all major economies have experienced significant contractions in 2020. The US has recorded a fall of 3.5% in GDP this year, Europe 4.3%, Japan 3.9% and bringing up the rear is the UK which has seen its economy contract by 9.7%.

The effect of the pandemic on the UK economy has been stark. It is an economy dominated by services and consumption and a significant reduction in activity in both sectors has driven this fall in GDP. Other more diversified economies have managed to weather this storm better, and only Spain (-9.1%) and Greece (-12.0%), with their reliance on tourism, have matched the UK result.

The Bank of England has recognised this and in early November extended their asset purchase programme by £150 billion to £895 billion. The Bank of England has more than doubled its programme this year, providing the market with significant levels of liquidity in the hope that loose monetary policy will provide a base for economic growth. Alongside this the UK Government continues to borrow at unprecedented rates to provide a fiscal stimulus to an otherwise moribund economy. Currently the UK Government has borrowed £206 billion this year. Last year it borrowed £35 billion.

As with all Governments around the world it is hoped that a combination of loose monetary policy and loose fiscal policy will mitigate some of the worst of the economic contractions. Without them we would have had a significant global depression. With it we are simply filling a demand driven hole in the economy and just about treading water.

Stimulus this is not, and loose monetary and fiscal conditions will have to remain in place for some time as economies gradually recover.

With bond rates around the world, at the short end, in negative territory there has never been a better time for Governments to borrow (they are being paid to do so!) and any talk of fiscal tightening to “pay back debt” risks any nascent recovery. Moreover, the market is currently not expecting these actions to be inflationary while demand and confidence remains weak.

Market reaction

Market reaction was swift to the news of the Pfizer vaccine with equity markets rising significantly on the news. These gains were further consolidated with the Moderna and Astrazeneca announcements.

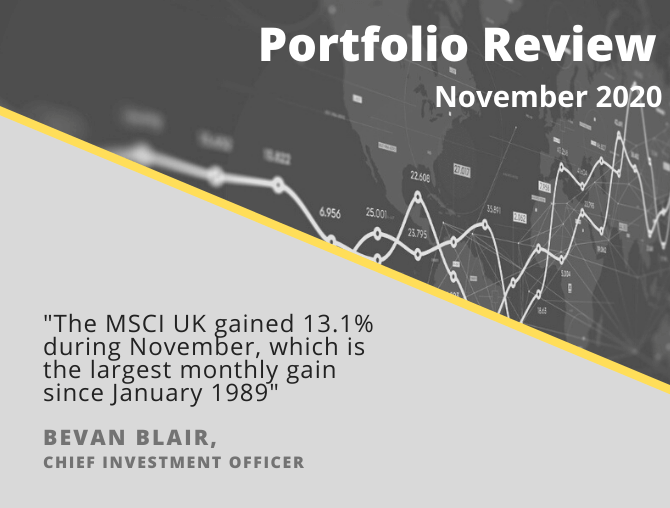

The MSCI UK gained 13.1% during November, which is the largest monthly gain since January 1989.

Stocks that had been badly beaten up during the year were the largest beneficiaries of market optimism. The main catalysts of the index moves were to be found in oil and gas, mining, and banking stocks. BP (+26%), Royal Dutch Shell (+33%), HSBC (+20%), Glencore (+36%) and Lloyds (+27%) led the way.

Tourism and leisure focused stocks also witnessed some very large gains, with IAG (the owner of British Airways) rising 60%, alongside EasyJet (59%), Cineworld (100%) and the Restaurant Group (58%). These stocks however have fared poorly this year and are all well below their 2020 peaks.

Around the world there was a similar story with equity markets rebounding strongly and “value” sectors performing the best. Sectors that had been pummeled recovered somewhat while others that had made significant gains during the year gave up some of these. The rotation has been quick and harsh but will probably not continue.

The US market gained 7.5% in sterling terms, Europe 13.6%, Japan 7.9%, Asia Pacific 5.6%, and Emerging Markets 5.8%. Overall global equities, as measured by the MSCI World Index gained 9.2%.

Corporate bond markets, both investment grade and high yield, also posted solid gains with sterling investment grade bonds gaining just under 2% and sterling high yield gaining just over 4%.

Gilt yields rose slightly with Gilts losing just one half a percent. Commodities had a strong month, especially industrial metals and oil and gas. Brent Crude rose from $37 a barrel to $47 a barrel, a 27% rise, reflecting renewed confidence in global demand in 2021.

Gold however suffered in November falling 5.5% in dollar terms. Sterling strengthened by 2.9% against the dollar and 2.6% against the Yen over the month, but was little changed against the Euro, reflecting little confidence in a good UK resolution in Brexit negotiations.

Portfolio comparison

Your portfolios all performed strongly over November and are now all in positive territory for the year. We gave up some relative performance as our underlying equity funds mainly ignore the sectors that have performed worst this year and therefore missed out on some of the rises.

| NOVEMBER | YEAR TO DATE | |||

| Active | Passive | Active | Passive | |

| Defensive | 1.99% | 2.32% | 1.06% | 0.86% |

| Cautious | 2.78% | 3.39% | 1.27% | 0.71% |

| Balanced | 4.37% | 5.51% | 2.38% | 1.31% |

| Growth | 5.66% | 7.33% | 2.31% | 0.55% |

| Adventurous | 7.13% | 9.32% | 3.02% | 0.23% |

The top 5 performers in the active portfolios were:

- Lindsell Train UK (+10.49%);

- Vanguard US Equity Index (+8.64%);

- Liontrust Special Situations (+8.25%);

- Lindsell Train Global Equity (+8.22%); and

- Evenlode Global Income (+7.94%).

The top 5 detractors were:

- Royal London Short Duration Gilts (-0.14%);

- Vanguard UK Short-Term Investment Grade Credit (+0.45%);

- TwentyFour Absolute Return Credit (+0.86%);

- M&G UK Inflation Linked Corporate Bond (+1.11%); and

- Troy Trojan Fund (+2.00%).

Find out how One Four Nine Portfolio Management invest here.

Dr Bevan Blair,

Chief Investment Officer,

One Four Nine Portfolio Management

London, Tuesday 15 December 2020.

All investment views are presented for information only and are not a personal recommendation to buy or sell. Past performance is not a reliable indicator of future returns, investing involves risk and the value of investments, and the income from them, may fall as well as rise and are not guaranteed. Investors may not get back the original amount invested.

All data is at 30 November 2020. One Four Nine Models are benchmarked against UK CPI and any other benchmark has been displayed for comparative purposes only and is not a benchmark for the Models. Performance figures are net of underlying fund fees and include One Four Nine Portfolio Management’s Management Fee of 0.24% (including VAT). All model portfolio performance data is sourced from One Four Nine Portfolio Management. All other data is from Bloomberg and Morningstar.

This service is intended for use by investment professionals only. This document does not constitute personal advice. If you are in doubt as to the suitability of an investment, please contact your adviser.

One Four Nine Group Limited Registered in England No: 11866793. One Four Nine Portfolio Management Limited is registered in England No: 11871594 and is authorised and regulated by the Financial Conduct Authority (FCA) FRN: 931954. One Four Nine® is a registered trademark.